Ecoinometrics' Friday edition analyzes the three most critical market signals impacting Bitcoin and macro assets. Bitcoin finally caught a break this week. Bitcoin has a much stronger foundation above $60K than it did just two weeks ago. Financial conditions are becoming less of a headwind for Bitcoin. June's inflation report came in better than expected.

USD index ended higher yesterday. Spot gold is down by nearly 3% this week. US weekly jobless filings fell to 208k (versus 217k expected), echoing a stabilising labour market, and retail sales eased amid lower energy prices. US Treasury yields were fairly muted yesterday, with the benchmark 10-year yield holding near 4.55%.

The iShares Expanded Tech-Software Sector ETF is headed for its sixth negative week in seven. The market no longer supports premium valuations without a reason to pay for them again. The chip sector controls the direction on Friday. The escalation with Iran shows no signs of abating.

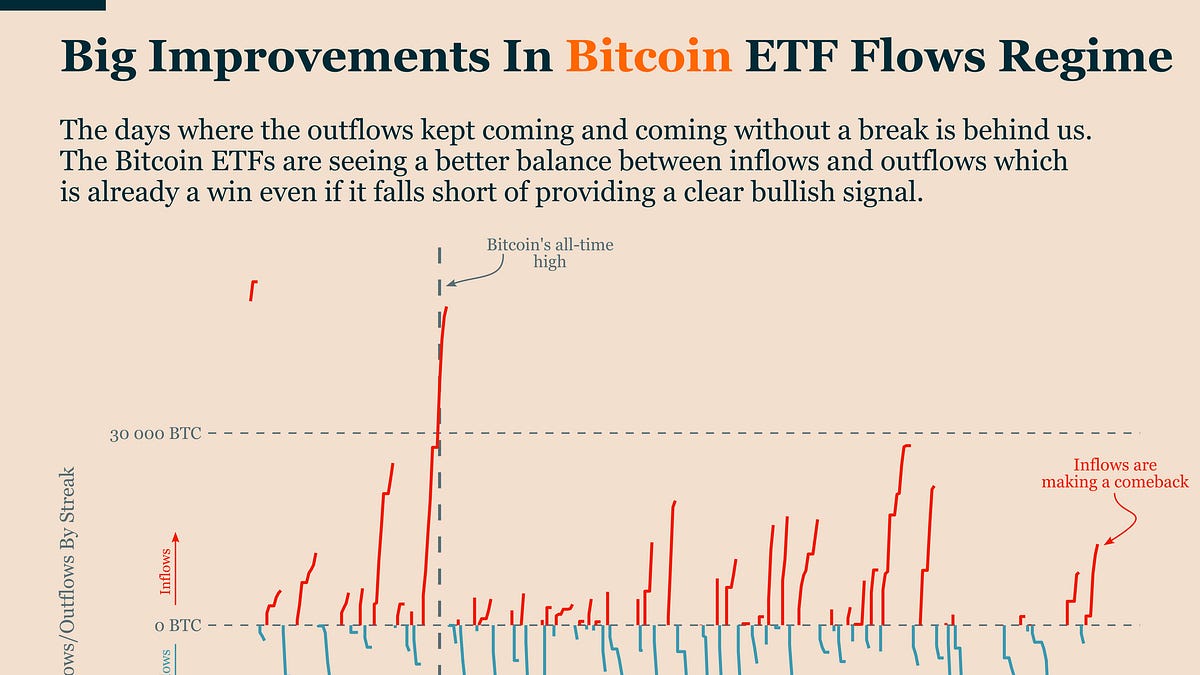

Long-term and short-term holders are selling into Bitcoin's recent rebound. Long-term holder realized-loss volume increased as Bitcoin approached $66,000. Short-term investors were selling into the same recovery for the opposite reason. US spot Bitcoin exchange-traded funds attracted money for three consecutive days.

Bitcoin price fell below $63,000 on Friday as a fresh wave of U.S. airstrikes on Iran and a new political dispute between Washington and Beijing pushed investors out of risk assets. Futures tied to the Nasdaq pointed to a decline of 1.6%, an echo of Thursday’s drop on Wall Street. Nikkei 225 dropped 4% and entered a correction, a fall of more than 10% from its June 25 peak, as memory-chip maker Kioxia lost 16.1%. Hong Kong's Hang Seng shed 2%, while the Shanghai Composite fell 3.1% to an 11-month low. WTI crude climbed near $79 a

iShares Expanded Tech-Software Sector ETF is headed toward its sixth losing week in seven. Alphabet is down in the pre-market session after declining on Thursday. Netflix is down on results that came in roughly in line. Intuitive Surgical dropped even after beating estimates and maintaining its full-year outlook. Alcoa slipped after cutting its 2026 alumina production forecast despite beating quarterly estimates. Verizon rose on plans to sell 274 retail stores and cut about 500 corporate jobs.

Copper prices are under short-term pressure due to slower growth in China, but the long-term outlook remains positive. The article examines the mixed economic data of China, tightening supply, inflation risks and the price levels that can determine the next move in copper prices.

Ecoinometrics' Friday edition analyzes the three most critical market signals impacting Bitcoin and macro assets. Bitcoin finally caught a break this week. Bitcoin has a much stronger foundation above $60K than it did just two weeks ago. Financial conditions are becoming less of a headwind for Bitcoin. June's inflation report came in better than expected.

USD index ended higher yesterday. Spot gold is down by nearly 3% this week. US weekly jobless filings fell to 208k (versus 217k expected), echoing a stabilising labour market, and retail sales eased amid lower energy prices. US Treasury yields were fairly muted yesterday, with the benchmark 10-year yield holding near 4.55%.

The iShares Expanded Tech-Software Sector ETF is headed for its sixth negative week in seven. The market no longer supports premium valuations without a reason to pay for them again. The chip sector controls the direction on Friday. The escalation with Iran shows no signs of abating.

Long-term and short-term holders are selling into Bitcoin's recent rebound. Long-term holder realized-loss volume increased as Bitcoin approached $66,000. Short-term investors were selling into the same recovery for the opposite reason. US spot Bitcoin exchange-traded funds attracted money for three consecutive days.

Bitcoin price fell below $63,000 on Friday as a fresh wave of U.S. airstrikes on Iran and a new political dispute between Washington and Beijing pushed investors out of risk assets. Futures tied to the Nasdaq pointed to a decline of 1.6%, an echo of Thursday’s drop on Wall Street. Nikkei 225 dropped 4% and entered a correction, a fall of more than 10% from its June 25 peak, as memory-chip maker Kioxia lost 16.1%. Hong Kong's Hang Seng shed 2%, while the Shanghai Composite fell 3.1% to an 11-month low. WTI crude climbed near $79 a

iShares Expanded Tech-Software Sector ETF is headed toward its sixth losing week in seven. Alphabet is down in the pre-market session after declining on Thursday. Netflix is down on results that came in roughly in line. Intuitive Surgical dropped even after beating estimates and maintaining its full-year outlook. Alcoa slipped after cutting its 2026 alumina production forecast despite beating quarterly estimates. Verizon rose on plans to sell 274 retail stores and cut about 500 corporate jobs.

Copper prices are under short-term pressure due to slower growth in China, but the long-term outlook remains positive. The article examines the mixed economic data of China, tightening supply, inflation risks and the price levels that can determine the next move in copper prices.